Retirement Planning

Protect & Plan for Your Retirement

5 Real Financial Risks

You Could Face in Retirement

We put a lot of time into saving and investing money for retirement, but we don’t spend nearly as much effort developing a strategy for withdrawing those assets once we retire. However, developing a retirement strategy is similar to planning a mountain trek — how we get down from the peak is just as important as how we scale up it. Once you stop earning a paycheck, asset growth may slow as you begin taking income. This is fine; it’s what you’ve been working for your whole life. But it is important that you develop a strategy to prudently draw down from that mountain of assets. Without a strategy, you could withdraw too much, too soon, and run out of money during retirement. This is a big part of retirement income planning: Choosing a reliable, methodical and flexible descent route. To do so, consider four questions that may influence the path you choose.

How Long Should I Expect to Live?

On average, a man who reaches age 65 can expect to live to age 84, while a woman can expect to live to 86. But those are statistical averages: Today, about one out of three 65-year olds will live until at least age 90, while one out of seven will reach age 95.

For a woman, the odds of outliving her husband are strong. Not only can she expect to spend more years in retirement, but she must prepare for the fact that medical and long-term care bills for her or her husband could impact her future income. An avalanche of expenses can potentially disrupt the financial confidence of a surviving spouse. This is one of many reasons why it’s important to consider all types of financial vehicles, including insurance options, to help ensure that a nest egg isn’t depleted due to long-term care expenses or the death of one spouse.

How Much Will the Cost of Living Increase During My Retirement?

Inflation can have a stronger impact on retirees compared with the rest of the population. That’s because retirees tend to spend a higher percentage of their household budget in categories that experience higher inflation, such as medical and long-term care.

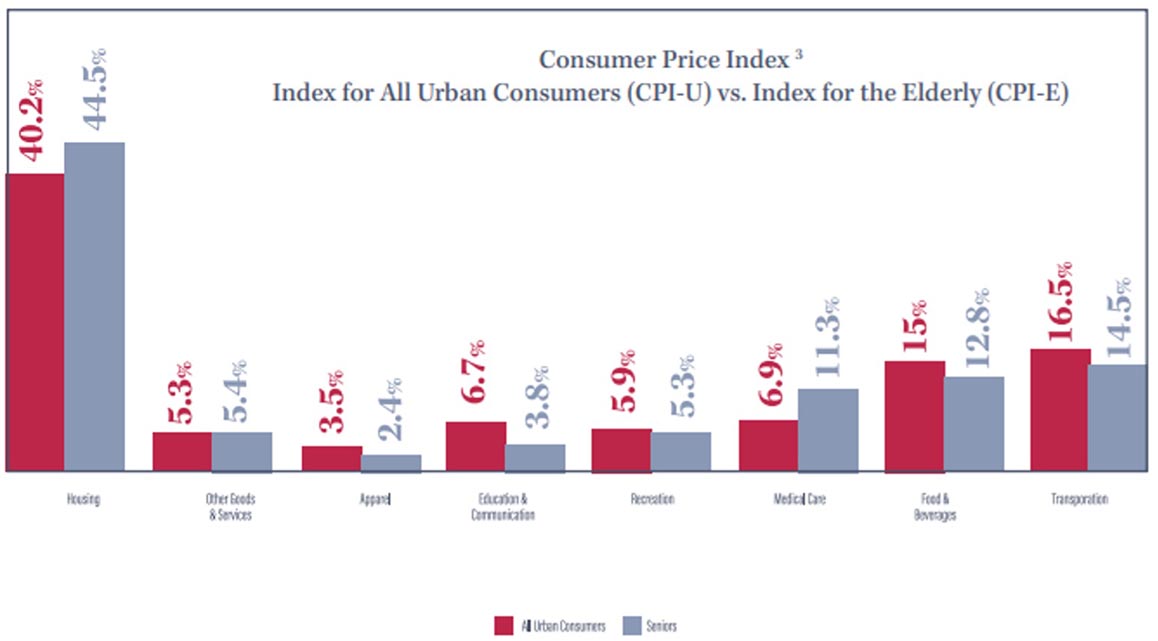

To help quantify the difference in cost-of-living expenses, the U.S. Bureau of Labor Statistics (BLS) periodically calculates an inflation index specifically for older adults, called the Consumer Price Index for Americans 62 years of age or older (CPI-E). While the BLS has not updated the index since 2011, the accompanying chart illustrates how the relative weights for housing and medical expenses are higher for older adults, indicating that a larger percentage of retirement income is spent in these areas.

To help determine long-term cost-of-living increases in retirement, consider areas in which you are likely to spend more as you age.

When Should I Consider Retiring?

Obviously, the age at which you retire depends on several variables, including if you enjoy your job and want to work past traditional retirement age and whether your health or your employer gives you a choice in the matter. However, another factor that not everyone considers is what could be going on in the investment markets when you’re nearing retirement. This is important because you typically want to avoid retiring just after or during a market decline.

When deciding when to retire, a key factor is the ability to be flexible. If market performance is in a period of decline, it may be prudent to delay retirement until the market recovers so that your portfolio does not suffer from an initial negative sequence of returns.

Where Should I Consider Placing My Assets?

As a general rule, retirees should transition some portion of their portfolio to more conservative accounts to help protect assets from market loss. Because there are a variety of circumstances that should be considered, it’s best to consult with an experienced financial professional to develop a tailored distribution plan. With that said, following is some general guidance to help you develop a financial strategy designed to last throughout retirement.

Determine how much income your portfolio needs to provide each year to supplement

Allocate a portion of assets to a liquid account to help pay for periodic expenses (such as homeowner’s insurance and property taxes) as well as an emergency fund.

- Consider whether it might be appropriate to continue investing a portion of your retirement portfolio for long-term growth opportunity to help offset the impact of inflation and the chances that you live a long time.

- Diversify equity investments to help minimize risk of loss.

- Be flexible with regard to your annual withdrawal rate; you may want to save excess money withdrawn in years when the market produces higher returns and reduce your withdrawal rate in down years — using those prior savings to supplement your income.

- Consider the value of repositioning a portion of your assets to an annuity to help secure a guaranteed income stream for both you and your spouse’s lifetime; this would help protect your income needs should the investment market experience a prolonged decline.

- Consolidate assets as much as possible for ease of management and automate required minimum distributions.

How Will You Descend?

For most people, it can take 30 years or more to accumulate a mountain of savings. Bear in mind that with today’s longer life expectancy, savings may need to last 30 years or more on the other side of the peak.

Your strategy for the descent should be slow and steady — the same way you accumulated those assets. Climbers use a rope and pulley system to control how quickly they rappel down a mountain. Likewise, at retirement you need the right tools and a predetermined route to help protect assets and draw them down in a controlled yet flexible manner, with the ability to make course changes as necessary.

Accumulating enough money for retirement is just half the journey; the other half is making that money last as long as you do. Schedule your consultation today to map out a detailed plan to help you confidently descend the mountain.